By Scott Bishop and Tom Mountain

Has 2020 given you whiplash? It feels like we’ve been in a storm for much of the year. And while the coronavirus pandemic is at its core a health issue, the downstream effects of it on other aspects of our society have been significant, perhaps the greatest being economic. Now that we’ve passed the mid-year point of 2020, it’s time for an update!

The Big Picture

Much of the economic data has been extremely negative, with record declines in employment, (1,2) and consumer spending. (3) The speed of the decline had no modern precedent. With government-imposed lockdowns and business closures, companies furloughed employees at a furious and painful pace. It is difficult to express in words, but it has been disheartening to see friends and family members sidelined from the workforce.

We are now in a recession, according to the National Bureau of Economic Research (NBER), the official arbiter of recessions and expansions. The prior expansion, which began in 2009, officially peaked in February, having lasted a record 128 months. In making its determination, the NBER concluded, “The unprecedented magnitude of the decline in employment and production…warrants the designation of this episode as a recession, even if it turns out to be briefer than earlier contractions.” (4)

The shortest recession on record lasted just six months and occurred in 1980. Second place: a seven-month recession in 1918-19, which was tied to the Spanish flu pandemic. There have been five recessions that lasted eight months, including the 1957-58 recession that coincided with the Asian flu pandemic. (5) While the economy is much different today, the recovery from the short, but steep 1957-58 recession was robust.

Given surprisingly strong data in May, April may mark the bottom of the economic cycle. If so, it will be the shortest recession on record. Let’s also acknowledge that the speed and depth of the decline have no modern parallels.

With massive support from the Federal Reserve, the federal government, and the reopening of previously closed businesses, employment in May unexpectedly surged to a record 2.5 million. (6) The private sector fared even better, with a gain of 3.1 million. (7) In June, the U.S. economy created 4.8 million jobs. (8)

Consumer spending, which fell a record 6.6% in March and a record 12.6% in April, rebounded by a record 8.2% in May. (9) Pent-up demand, stimulus checks, generous unemployment benefits, a rise in employment, and reopened businesses supported sales. Consumer confidence is also improving per the Conference Board’s Consumer Confidence Index. (10) It remains well below pre-coronavirus levels, but rising confidence and re-openings are supportive of economic activity.

Still, not all is rosy. And a strong recovery is not assured, as visibility remains incredibly limited.

Layoffs, as measured by first-time jobless claims are slowing but remain at unusually high levels. (11) The weekly layoff numbers have been more than double what we saw at the peak of the 2007-09 recession. (12)

Forecasting In Today’s Environment

In his testimony before the House Committee on June 30, Fed Chief Powell said, “Many businesses are opening their doors, hiring is picking up, and spending is increasing. Employment moved higher, and consumer spending rebounded strongly in May. We have entered an important new phase and have done so sooner than expected.” (13) But he also recognized the need to keep the virus in check. “The path forward for the economy is extraordinarily uncertain and will depend in large part on our success in containing the virus. A full recovery is unlikely until people are confident that it is safe to re-engage in a broad range of activities,” Powell added.

We are seeing a spike in Covid-19 cases in many states, which is creating a new round of uncertainty. It has fueled choppier day-to-day activity in the market. Yet, at least so far, the bull market seems to be coexisting with the rise in cases. Despite higher infection rates, deaths continue to trend lower. This reduces fear somewhat and in turn reduces odds of new lockdowns.

U.S. Treasury Secretary Steven Mnuchin took a more optimistic tone in his testimony with Powell. “The Blue Chip Report is forecasting that our GDP will grow by 17% annualized in the third quarter, and by 9% in the fourth quarter,” which follows what is expected to be record contraction in Q2. Mnuchin also expects significant progress on the employment front. (14)

V-, U-, L- Or W-Shaped Recovery

Economists give economic recoveries what might be called a letter grade when discussing possible paths. It’s not the traditional A through F scale. Instead, the letter intuitively describes the shape of the recovery.

A V-shaped recovery would be ideal, as it would represent a robust bounce. Might we get a V? Data in May was unexpectedly strong and cautiously encouraging. However, even during what we might consider more normal times, forecasting is difficult. Today, there’s no playbook and no framework to model outcomes.

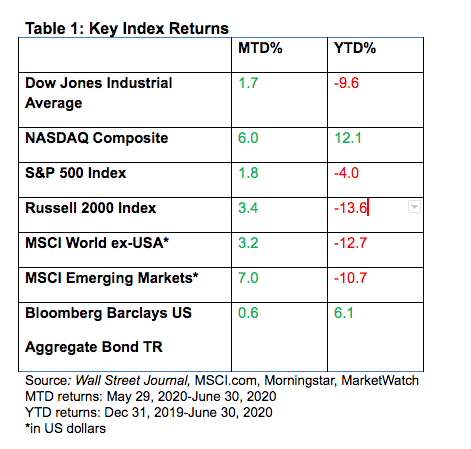

We could give you several reasons to see a strong rebound unfolding. We could also give you several reasons why a sluggish recovery might take place. The strong rebound in stocks since the late-March low is astounding, especially given the economic damage. It suggests the collective wisdom of investors is more optimistic. Fed support, rock bottom interest rates, the reopening trade, and stronger economic data have helped. We also believe investors are looking past this year’s hit to corporate profits and are expecting an upturn in 2021. The jump in daily cases has created some renewed volatility, and it bears watching, but it has yet to knock the bulls off course.

Ultimately, the path of the virus will play the biggest role in how the economic outlook unfolds. Some folks are itching to get back to normal, while others remain on guard against the disease and are taking a more cautious approach. It may take time for some businesses to fully recover. Some never will. Investors are betting that an economic bottom is in sight. Try to look past continued volatility. However, based on recent economic reports, we think we hit that bottom in April.

Financial Planning Lessons From The COVID-19 Crisis

None of us expected an economic upheaval spawned by a health crisis as the year began. As we discuss some of the lessons and takeaways from the COVID-19 crisis, you’ll probably recognize some of the themes. Let’s not forget that the fundamentals–the core financial precepts–are always the building blocks of any credible financial plan.

Money At The End Of Your Month.

Saving for an emergency cannot be underestimated. Having three to six months worth of expenses saved is optimal and will help you achieve an added benefit–financial peace of mind.

It’s reflected in the proverb, “The borrower is servant to the lender.” (15) It’s not that we would counsel against a mortgage for a home or a reasonable loan for a car. But accumulation of wants (not needs) with debt doesn’t bring contentment. Instead, it brings stress. We have seen it over and over. You want money at the end of your month, not month at the end of your money.

A financial cushion eliminates one of life’s worries.

Wants Versus Needs

Many of us have learned to do without certain things during quarantine. Whether we wanted to or not, we were forced to cut back on things.

Ask yourself this question, “As businesses reopen, are there things I can do without? Can I continue to cut back and still maintain my lifestyle?” Many of our entertainment options have been curtailed. As we emerge from our homes and businesses reopen, are there items that can be trimmed from the budget?

It’s not a cold turkey approach, i.e., no more eating out, sporting events, travel, or theater. But can we reduce expenditures on some items without sacrificing our overall lifestyle? You might be surprised at how small changes add up over time.

Diversification And Tolerance For Risk

We’ve just witnessed an unusual amount of stock market volatility. Calling it a rollercoaster does not fully capture the experience. The major indexes have erased much of their losses, but how did you fare emotionally when stocks took a beating? Now is the time to reevaluate your tolerance for risk. We’d be happy to assist and make any adjustments as they relate to your longer-term financial goals.

Expecting The Unexpected

From its March 2009 low to the February 2020 high, the bull market ran for over 10 years. (16) We know bear markets are inevitable, but I recognize that the onset of a steep decline may be unnerving. Nonetheless, a well-diversified portfolio of stocks has historically had an upside bias. That upside bias is incorporated into the recommendations we make, even as our recommendations are tailored to your individual circumstances and goals.

Further, a healthy mix of fixed-income helped cushion the decline. While we monitor events and the markets over a shorter-term period, let’s be careful not to take our eyes off your longer-term goals.

Be Proactive, Not Reactive

The steps above are a broad overview and individual circumstances may vary. Taking inventory is critical and it’s half the battle. Be proactive, not reactive. You may find you are in a much better position than you realized. As always, we are here to help. We hope you’ve found this review to be helpful and educational.

We understand the uncertainty facing all of us. We are grappling with an economic and a health care crisis. It’s something none of us have ever faced. We have addressed various issues with you, but we have an open-door policy. If you have questions or concerns, let’s have a conversation. That’s what we’re here for. Reach out to us at 562-432-3783 or [email protected].

As always, we are honored and humbled that you have given us the opportunity to serve as your financial advisory team.

About Us

Mountain-Bishop Private Wealth Management is a full-service independent financial services and investment services firm that has been providing retirement and investment guidance to high-net-worth individuals, business owners, and Boeing employees for more than 25 years. Through our long-term guidance, we strive to help our clients build, protect, distribute, and transfer their wealth, tailoring our services and strategies to address each client’s unique needs so they can bridge the gap between their current financial situation and their long-term goals.

Scott and Tom built their practice on trust and excellence. They focus individually on each client, delivering the personalized touch that is missing with many other firms.

The Financial Consultants of Mountain-Bishop Private Wealth Management are registered representatives with, and securities and advisory services offered through LPL Financial, a registered investment advisor, Member FINRA/SIPC. For hyperlinks to FINRA/SIPC, please refer to “See Contact Info” section above.

The LPL Financial Registered Representatives associated with this site may only discuss and/or transact securities business with residents of the following states: (AK, AZ, CA, CO, FL, GA, ID, IL, MI, MO, NC, NJ, NM, NV, OR, PA, SC, UT, VA, WA) SCOTT E. BISHOP CA LICENSE OB55872 THOMAS P. MOUNTAIN CA LICENSE OB55827

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual. All performance referenced is historical and is no guarantee of future results. All indices are unmanaged and may be invested into directly.

The economic forecasts set forth in this material may not develop as predicted and there can be no guarantee that strategies promoted will be successful.

________________

(2) https://www.bls.gov/news.release/pdf/empsit.pdf

(3) https://www.bea.gov/data/consumer-spending/main

(4) https://www.nber.org/cycles/june2020.html

(5) https://www.nber.org/cycles.html

(8) https://www.bls.gov/news.release/pdf/empsit.pdf

(9) https://www.bea.gov/data/consumer-spending/main

(10) https://www.conference-board.org/data/consumerconfidence.cfm

(13) https://www.federalreserve.gov/newsevents/testimony/powell20200630a.htm

(14) https://financialservices.house.gov/uploadedfiles/hhrg-116-ba00-wstate-mnuchins-20200630.pdf

(15) Proverbs 22:7